(Bloomberg) — When crude surges above $90 a barrel and the leaders of Saudi Arabia and Russia get on the phone to congratulate each other on a job well done, oil consumers should take note.

Most Read from Bloomberg

After half a year in the doldrums, the price of the world’s most important commodity is on a tear as the biggest players in OPEC+ get serious about making sure supply doesn’t exceed demand. The 1 million barrel-a-day output cut the Saudis initially pledged solely for the month of July will now be in place until year-end, alongside a smaller export reduction from Russia.

It’s not just the size of the supply deficit likely to result from this — about 2.7 million barrels a day in the fourth quarter according to Rystad Energy A/S — that should worry consumers. It’s the fact that the West’s somewhat-estranged ally Riyadh, and its outright foe Moscow, are now bound so firmly together in their push for higher prices.

“Crude tightness seems quite legitimate and quite real,” said Greg Sharenow, managing director at Pacific Investment Management Co. “This certainly keeps oil markets on the boil.”

Saudi Arabia is squeezing the market just as consumption surges. Global oil use reached a record 103 million barrels a day in June, according to the International Energy Agency. The following month, the kingdom reduced production to a two-year low of about 9 million barrels a day.

Russia’s extra cut is less than a third of the size of Riyadh’s and applies to exports rather than production, but their combined effect is forcing consumers to run down their inventories to satisfy demand, driving up prices in the process.

Since July 1, international crude benchmark Brent has risen about 20%. The price in New York of diesel, a vital fuel to keep the global economy ticking over, has jumped by a third.

This summer surge in fuel costs gives Russia extra funds to prosecute its war in Ukraine and Saudi Arabia more cash for its investment priorities. It also threatens a fragile global economy with a renewed inflationary spike, potentially derailing central banks’ plans to ease back their cycle of interest-rate hikes.

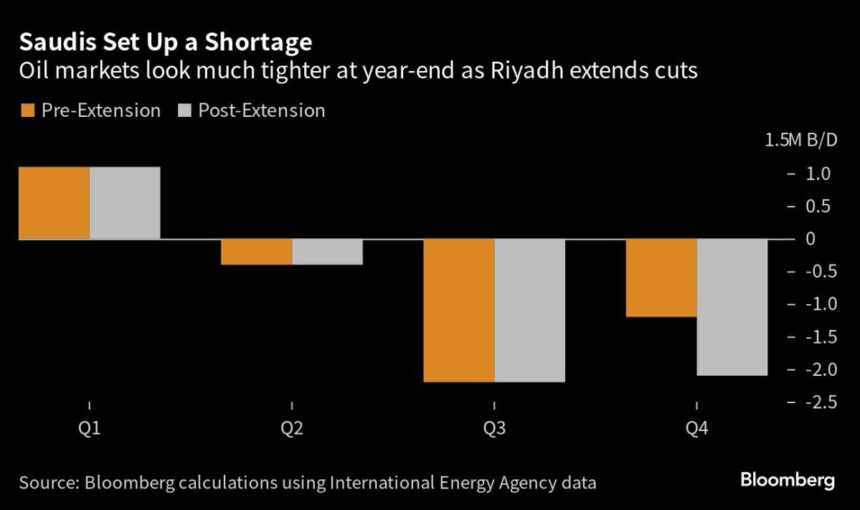

There had been some hope that the changing of the seasons would ease the tightness in oil markets. Forecasts from the Paris-based IEA, which advises major economies on energy policy, indicated a supply deficit of just over 1 million barrels a day in the fourth quarter, half as deep as the estimated shortfall from July to September.

Tuesday’s joint announcement from Saudi Arabia and Russia shifted that outlook markedly, making the estimated deficit in the final quarter just as severe as over the summer. This means even higher oil prices worldwide, according to Oslo-based consultant Rystad Energy.

“Our supply-demand model shows some hefty deficits,” said Emily Ashford, a commodity analyst at Standard Chartered Plc. “A cut by Saudi Arabia has a lot more clout than purported cuts elsewhere — when they say they will do it, they really mean it.”

Supply Alternatives

So what chance does the world have of avoiding a damaging oil price spike?

When it announced the extension of its cuts, Saudi Arabia did say it would review the decision every month and could increase production if necessary. But observers of the kingdom say consumers shouldn’t expect it to change its mind this year.

“Riyadh is content with its market management and with the price,” said Raad Alkadiri, managing director of energy, climate and resources at Eurasia Group. “There was little likelihood it was going to loosen supply this year and risk a fall in prices given uncertainty over demand in China persists.”

There are other potential sources of extra supply from the Organization of Petroleum Exporting Countries, but they all face plenty of hurdles.

Iraq could add 400,000 to 500,000 barrels a day of production if it solves a three-way legal dispute with its semi-autonomous Kurdish region and the government of Turkey that shut down a key export pipeline. Yet after six months of talks a resolution is still proving elusive.

Iran has been boosting production amid weaker enforcement of US sanctions, but its exports may have reached their peak for the year.

“The White House already enabled more Iranian barrels onto the market as part of the diplomatic deal,” said Helima Croft, head of global commodity strategy at RBC Capital Markets. “With Iran already nearing pre-sanctions production levels, the question is how much more is left in the Iranian tank.”

Consumers’ Choices

US President Joe Biden, who is up for reelection next year, has another potential tool at his disposal to curb prices — the Strategic Petroleum Reserve. Its resources were tapped enthusiastically last year with a historic drawdown of about 180 million barrels. Yet when crude prices dropped earlier this year, the process of refilling began.

In theory, the Department of Energy says it could still conduct a competitive sale, award contracts and prepare to begin deliveries within 13 days of a presidential order to tap the SPR. In reality it could take longer due to aging facilities and pipelines. The current refill plan is already set to take years to complete.

On the consumer side of the supply-demand equation, the greatest prospect of avoiding an oil spike may lie in China. The country’s sluggish economy has been a drag on prices for the much of the year, with little sign of a major economic turnaround despite Beijing’s efforts to stimulate growth.

If oil demand in the world’s largest importer were to fall well short of forecasts, the fourth-quarter supply deficit would also shrink. Chinese macroeconomic sentiment is a potential downside risk, said Rystad, but the latest mobility indicators do not show an imminent deceleration.

Energy Aspects Ltd. analysts including Amrita Sen and Jianan Sun, citing their first trip to China since the pandemic, were even more blunt.

“The western view of Asia, particularly China, couldn’t be further from reality,” they said in a note. “End-user demand and refinery runs are strong, and every Chinese energy company we met with noted how oil demand has completely decoupled from economic data.”

After many months in cheaper crude was helping the fight against inflation, this leaves consumers facing a new market paradigm.

“Oil prices have reached levels at which they will impact headline inflation,” said Christof Ruhl, an adjunct senior research scholar at the Center on Global Energy Policy at Columbia University. “This is not only something Biden will not like, but this is something the Fed may have to react to.”

Most Read from Bloomberg Businessweek

©2023 Bloomberg L.P.