The U.S. stock market doesn’t deserve to fall as much as it has because of higher interest rates alone — and soon investors will begin to act on this realization.

The conviction that stock prices fall when interest rates rise is so universally held that few stop to examine it. But unexamined and untested beliefs can all too easily lead us astray. As Humphrey Neill, the father of contrarian analysis, constantly reminded his clients: “When everyone thinks alike, everyone is likely to be wrong.”

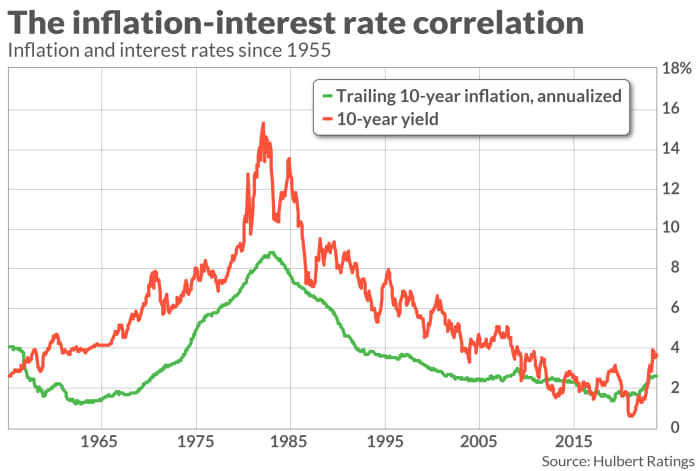

The first step in a re-examination is to remind ourselves that interest rates and inflation are highly correlated. This has been true historically, as you can see from the accompanying chart.

This year has been no exception: The 10-year Treasury yield

BX:TMUBMUSD10Y,

which many single out as the culprit in why the bull market has stopped in its tracks, has risen sharply, to 4.81% from 3.79%, since the start of 2023 through Oct. 3. Over the same period, the 10-year breakeven inflation rate — bond investors’ collective best judgment of expected inflation over the next decade — has risen slightly to 2.33% fro.m 2.26%

The interest-rate/inflation correlation is crucial, because nominal corporate earnings grow faster when inflation is higher. That doesn’t mean investors should welcome inflation, since higher inflation also means that future years’ earnings must be discounted at a higher rate.

But for many behavioral reasons, investors place greater weight on the negative impact of the greater discount rate than on the higher nominal earnings-growth rate that typically accompanies higher inflation.

Economists refer to this investor error as “inflation illusion.” Perhaps the seminal study documenting how this error impacts the stock market was conducted by Jay Ritter of the University of Florida and Richard Warr of North Carolina State University. They found that investors systematically undervalue stocks in the presence of high inflation.

Investors will make the same error, in reverse, when inflation and interest rates start to come down. That’s why the foundation of a major buy signal is currently being built.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com

More: Stock market likely to correct if 10-year Treasury yield reaches 5%, RBC says

Plus: How rapidly rising Treasury yields are shaking up financial markets — in 5 charts