After more than a decade of steady growth, the US pet market has faced a variety of complex challenges in recent years. From the uncertainty of the pandemic to the upheaval caused by sky-high inflation and rising interest rates, it’s been quite a roller coaster, as Shannon Landry Brown, the Pet Brand Manager for Packaged Facts, explained.

After more than a decade of steady growth, the US pet market has faced a variety of complex challenges in recent years. From the uncertainty of the pandemic to the upheaval caused by sky-high inflation and rising interest rates, it’s been quite a roller coaster, as Shannon Landry Brown, the Pet Brand Manager for Packaged Facts, explained.

Earlier this week, Shannon led an in-depth and data-packed webinar titled “US Pet Market Outlook 2024: Opportunities in a Mixed Growth Landscape,” which featured a distinguished panel of long-time Packaged Facts analysts including David Sprinkle and David Lummis.

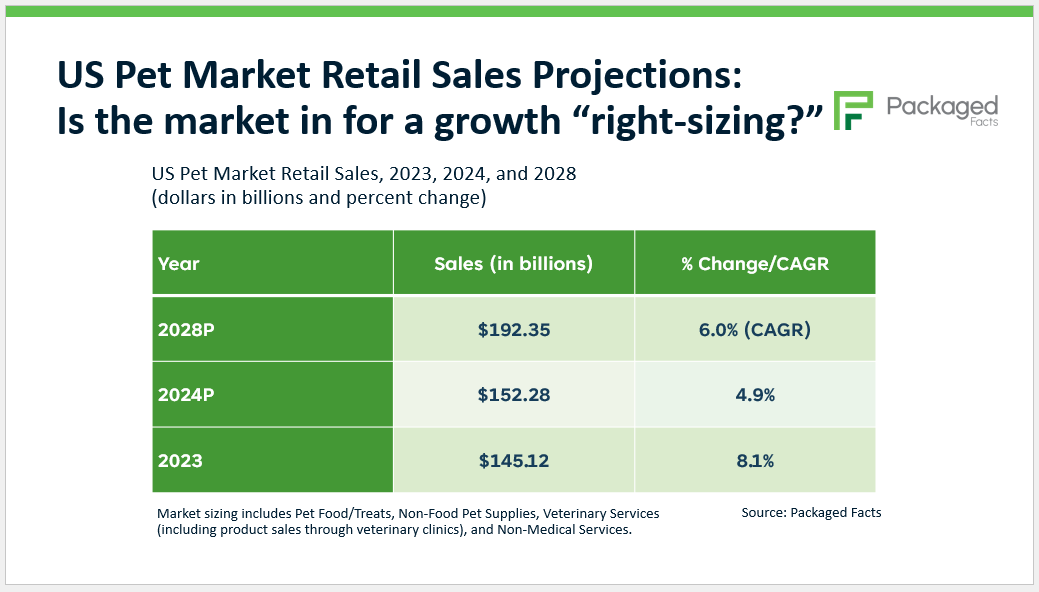

The webinar discussed several significant trends shaping the $145 billion US pet industry. In this article, we’ll recap the important points from the webinar to give you insights into where the pet market is headed. You are also welcome to watch the pet webinar in its entirety.

1. Impact of Inflation on Pet Owner Spending

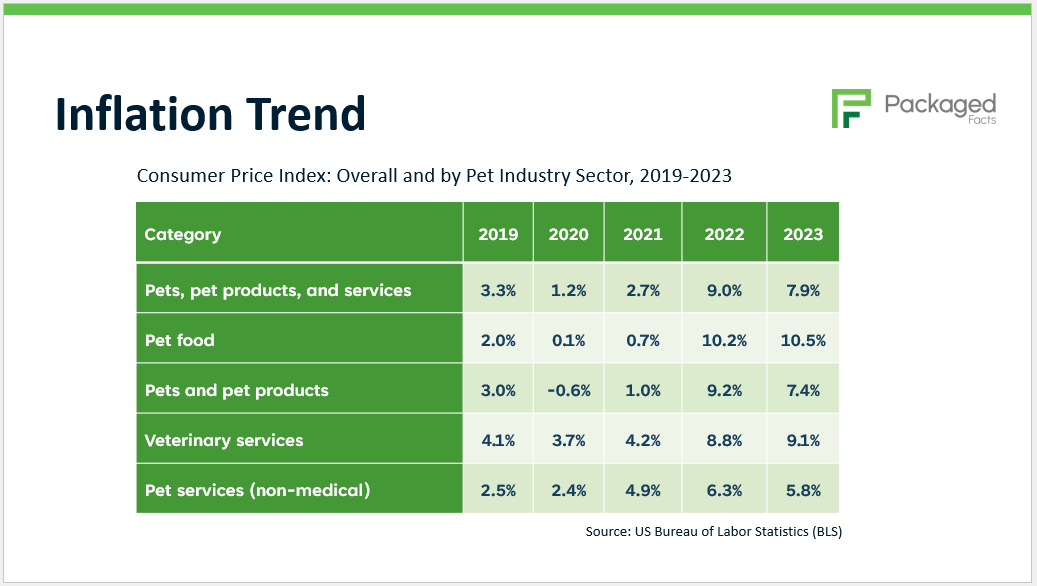

“The impact of the pandemic obviously didn’t end with the retreat of COVID, and one of the more unpleasant surprises of the post pandemic era has been the spike in inflation,” David Lummis said. “So much of the growth over the past two or three years has been inflation related.”

Across all pet market categories in 2022 and 2023, the rate of inflation was double or triple the rates of previous years, based on changes in the Consumer Price Index.

In most pet market categories, most or all of the dollar advancements of 2022 and 2023 were inflation-related as opposed to “real.”

In Packaged Facts’ January 2024 Survey of Pet Owners, 31% of pet owners reported that their ability to buy non-essentials had been negatively impacted by the economic environment, and 31% said their ability to pay their monthly bills was negatively impacted.

“That’s a fairly dramatic proportion of the market,” David Lummis noted. “A good long-term strategy for the market is probably not to simply rely on the willingness and the ability of affluent households to spend more but to also draw in some of those lower income households.”

In the past, premiumization was a major driver of the market, but inflation is raising the bar even higher, creating a “storm of affordability concerns.”

To convert pet owners to higher priced products in the future, pet marketers will have to emphasize good value and offer compelling pet health benefits as well.

2. Economic Challenges Facing Younger Pet Owners

Younger pet owners are essential to the future of the pet industry. As more baby boomers age and eventually give up pet ownership, it’s critical for younger generations to move into the market to help maintain steady levels of demand.

However, younger consumers are facing significant barriers to pet ownership, as Shannon explained:

- Credit crunch: Younger pet owners are more likely to have credit card debt compared to baby boomers and gen Xers. Younger pet owners are also more likely to live paycheck to paycheck and use options to buy now, pay later. This lack of disposable income makes the cost of pet ownership a challenge.

- Return of student loan payments: The resumption of student loan payments also had a major impact on disposable income. About 6.6 million or 10% of pet owners overall have student loans, rising to 15% of millennial pet owners. As these consumers grapple with the burden of student loans, they may cut back on non-essential products, trade down to lower-cost brands, and seek alternatives to costly veterinary services as well.

- Housing patterns: Dog ownership has a strong correlation with the type of housing people have. Homeowners are 68% more likely than renters to have dogs. In the current economy, home ownership has become more out of reach for first-time buyers, due to increasing rents, high mortgage rates, and a shortage of housing stock. This could negatively impact the pet market, as fewer households adopt dogs.

3. Shift to Lower-Cost Pet Products and Services

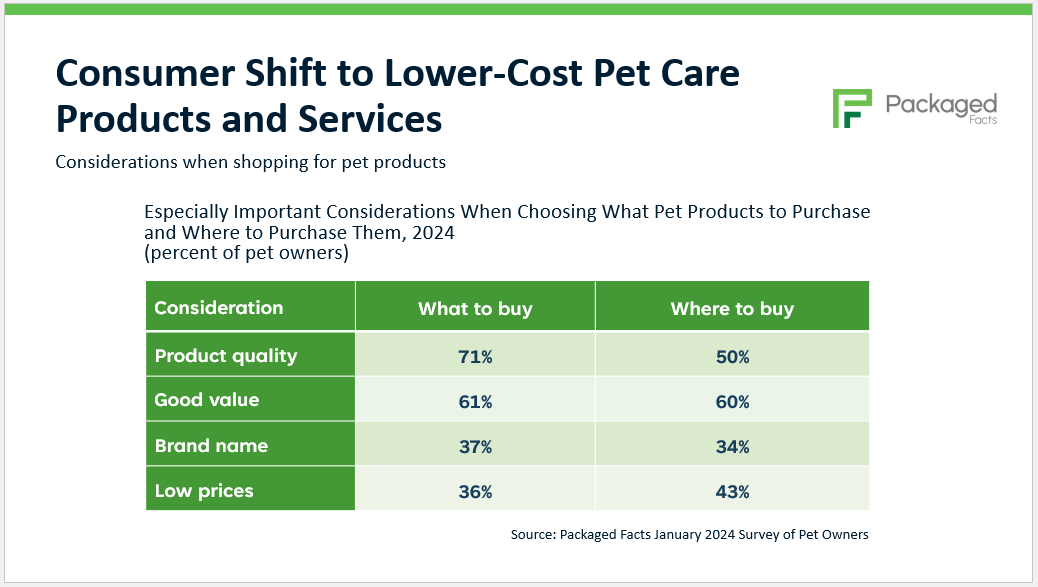

While many consumers are seeking to economize, it’s important to note that pet owners do not want to sacrifice quality to do so.

Packaged Facts survey results from January 2024 show that product quality is a prime consideration for 71% of pet owners when deciding what to buy. Good value is almost equally important, cited by 61% of pet owners for what to buy, compared to only 36% of pet owners citing low prices as impacting what they buy.

To save money, some pet owners are trading down to lower-priced brands in pet food. Packaged Facts survey results from January 2024 show that among pet owners who had switched pet foods in the past year, 32% of dog owners and 28% of cat owners had switched to a lower-priced brand.

In line with this trend, the usage of private label products is also on the rise, creating a significant opportunity in the pet market. “From a global perspective, the private label usage rates in the United States are still far below those in most Western European countries, and that suggests a lot of potential to my mind,” according to David Lummis.

As pet owners seek to save money where they can, pet services continues to offer a mixed outlook. Although boarding and daycare services have rebounded since the pandemic, more discretionary areas such as grooming and training have yet to fully recover. Veterinary services is also down disproportionately to pet ownership.

However, one bright spot is the healthy growth of pet insurance and veterinary expense plans, which cater to mid-range and lower-income households that need more help paying vet bills. Pet insurance has increased its customer base 29% from 2021 to 2023.

4. Decline in the Dog Population

“Flat-to-declining dog population patterns have chipped some of the bedrock off real (excluding inflation) pet industry dollar growth,” David Sprinkle explained. Several factors are at play including generational shifts in pet ownership, the cost of pet ownership, and slowing US household growth overall.

From 2019 to 2023, the number of dog-owning households fell by 5% from 52.5 million to 49.9 million, with numerical declines across all generational cohorts from millennials to pre-boomer older seniors. Growth of 5% in the cat-owning household base from 30.6 million to 32.1 million only partially offsets these losses.

“I think it’s worth saying that from a global perspective, there’s nothing in the human DNA which says that the pet market has to be as dog centric as it is as it has been in the US, and we do see the major US marketers, watching the numbers, and sort of shifting gears a bit,” David Lummis adds.

5. Continued Pet Industry Growth Amid Challenges

Taking a cautiously optimistic approach, Packaged Facts predicts 2024 US pet market growth approaching 5%, with some categories, such as durable products having a harder time. Longer term, through 2028, the market will see a 6% compound annual growth rate (CAGR).

“The pet market is in good shape, by any normal consumer market standard,” David Sprinkle concluded. “A lot of mature, huge consumer markets—in packaged goods, for instance—would kill for a 6% CAGR projected over the next five years. It’s only in relation to how sort of spoiled we were before the pandemic that the current numbers look like mixed growth.”

Additional Pet Industry Market Research

For more information, watch for the soon-to-be-released report US Pet Market Outlook, 2024-2025 from Packaged Facts, which analyzes current and projects future retail sales and trends across the US pet industry.

In addition, Packaged Facts has published a variety of other pet industry market research reports that may interest you including:

About Packaged Facts

Packaged Facts, a division of MarketResearch.com, publishes market intelligence on a wide range of consumer market topics, including consumer demographics and shopper insights, the food and beverage market, consumer financial products and services, consumer goods and retailing, and pet products and services. Packaged Facts also offers a full range of custom research services. Reports are also available for purchase through MarketResearch.com.