MBW Reacts is a series of analytical articles from Music Business Worldwide written in response to major recent entertainment events or news stories.

Spotify announced last Monday (July 24) that it was upping the price of its subscription packages in 53 markets. The timing of this move wasn’t random.

A day later, on July 25, SPOT announced its Q2 2023 results.

Most Q2 key metrics from a music industry standpoint – particularly the platform’s number of global subscribers (+10m QoQ) – were satisfactory or better-than-satisfactory.

But Spotify investors weren’t happy with some of the firm’s more commercial metrics in Q2, particularly quarterly revenues (€3.18bn), which came in €30 million below analyst estimates.

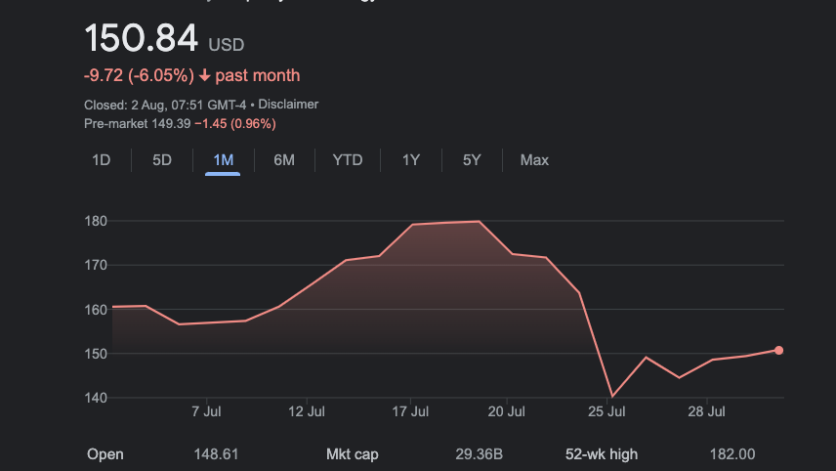

That revenue miss sent Spotify’s stock tumbling, down over 14% at close on the NYSE last Tuesday.

If that subscription price rise announcement last Monday was designed to fluff Spotify’s share price – offsetting an inevitable fall, post-earnings, the following day – it didn’t work.

At the time this article publishes (August 3), SPOT’s stock price stubbornly remains 11%down on its value at the start of last week.

Spotify’s share price movement over the past month – note tumble on July 25 (source: Google Finance)

As MBW’s previous number-crunching has shown, Spotify’s new price lifts – effective immediately – stand to grow the company’s revenues in the US alone by somewhere between USD $247 million and $533 million annually.

But could Spotify now make an even bolder move to try and boost subscription revenues in the United States?

Could it consider eliminating its free tier, and forcing its current ‘free’ users to pay for a subscription, or give up their use of the platform entirely?

Such a move has started becoming popular in music streaming circles: loss-making ad-supported streaming tiers have recently been cut by the likes of Gaana, Resso (now TikTok Music), and Deezer across multiple markets.

So what about the world’s largest subscription music service – Spotify – following suit in the world’s largest music market, the USA?

The idea has been suggested to MBW by a couple of high-profile music industry execs over the past couple of months. And there are certainly strong arguments why Spotify might be encouraged to do so at some point over the next few years (which we’ll get into shortly).

However, as we’re about to demonstrate, the commercial case for doing so today is… debatable.

First, then, let’s get into the math. Warning: it’s hairy stuff, and it requires a fair bit of prep to set the scene.

Credit: Haithem Ferdi

The prep work

So: What impact could a free tier shutdown have on Spotify’s revenues in the States?

Answering this question is harder than it might be, owing to missing information in Spotify’s SEC filings. But we can still have a decent crack at it to get us in the ballpark.

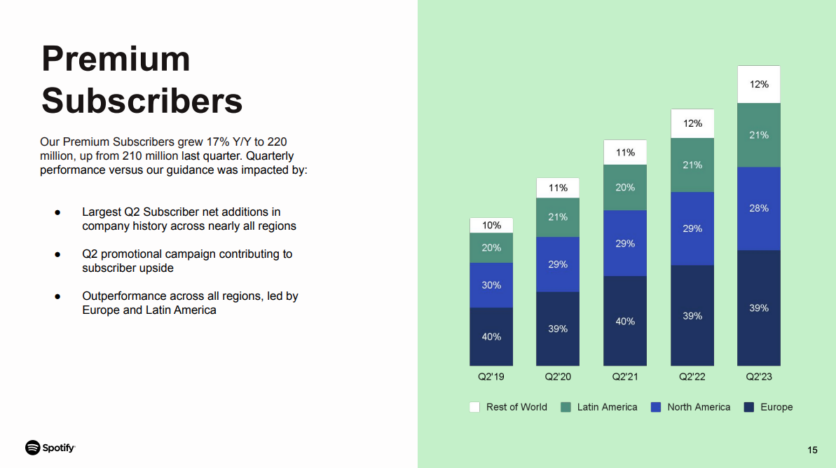

As of the close of Q2, according to its SEC filings, Spotify had 220 million paying subscribers globally, of which approximately 61.6 million (28%) were based in either the US or Canada (‘North America’).

Source: Spotify Q2 2023 investor presentation

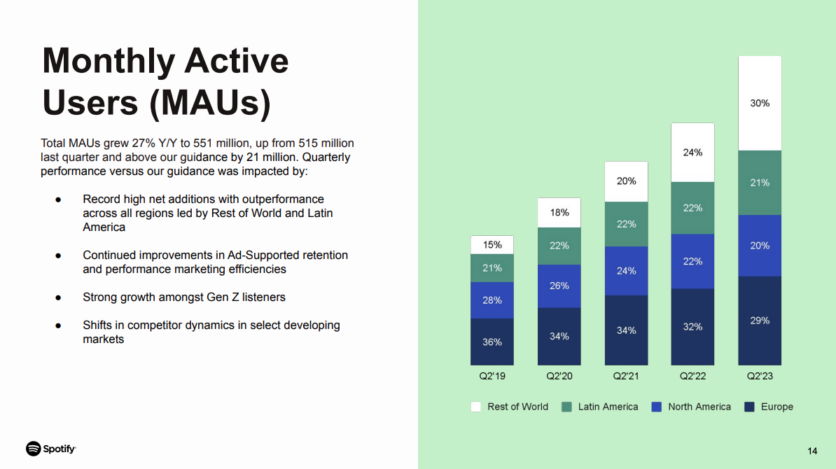

SPOT also counted 343 million ad-supported MAUs (i.e. free Monthly Active Users) globally at the same point.

Annoyingly, the company doesn’t provide a geographical breakdown of these ad-supported MAUs, but it does publish one for overall MAUs (i.e. active paying subs plus active free users).

Spotify’s total MAUs at the close of Q2 (subs plus free active users) stood at 551 million, and 20% of this number, according to the company, were based in either the US or Canada.

Source: Spotify Q2 2023 investor presentation

We can do a bit of rough math here to work out approximately how many free users Spotify has in North America.

Here goes: 20% of 551 million gives us the total number of paying and non-paying Spotify MAUs in the US and Canada. That’s 110.2 million.

If we then subtract from this number the approx number of paid-for Spotify subscribers in these regions (61.6m), we end up with 48.6 million.

That’s roughly the number of active free users on Spotify at the close of Q2 in the US and Canada.

(Sidenote for the eagle-eyed mathematicians out there: Spotify’s Q2 2023 number for its global ad-supported MAUs (343m) added together with its global Premium users (220m) doesn’t perfectly add up to its given number for total global MAUs (551m vs. 563m). That’s because Spotify’s stated Premium subs number includes a relatively small number of subscribers who paid for the service in the period, but who weren’t active (i.e. weren’t MAUs). The difference is not material for the rough sketch we’re about to embark upon.)

To recap, then: there were somewhere around 48.6 million non-paying Spotify users in North America in Q2 2023 vs. around 61.6 million paying subscribers in the same territories.

Unhelpfully, Spotify’s SEC filings also fail to offer a breakdown of global markets in terms of the revenue generated on its service – both for Premium subs, and for ad-supported users.

For this reason, we’re going to have to rely on the two below assumptions to push our math along, based on educated guesswork via published industry/company numbers:

Assumption 1:In Q2 2023, Spotify generated USD $220 million from ads in North America.Basis for this assumption: In its Q2 fiscal rundown, Spotify confirms that it EUR €404m (USD $440m) in global ad-supported revenue, including podcasts. We’re assuming that North America (US and Canada) were jointly responsible for a full 50% of that figure. Why? The IFPI’s latest Global Music Report shows the US and Canada jointly generating just shy of half (49%) the record industry’s $2.9 billion wholesale revenue generated via ad-supported audio platforms globally in 2022.

Assumption 2:Spotify’s Premium monthly ARPU in the months ahead in the United States (including all individual Duo/Family Plan users) will be USD $5.12.Basis for this assumption: Spotify’s published monthly ARPU figure for Premium subscribers is significantly lower than the real number in the United States (with so-called ‘emerging markets’ naturally pulling the global figure down). However, it’s a useful ‘floor’ / conservative figure for us to use. In Q2 2023, according to its SEC filings, Spotify’s Global Premium monthly ARPU was €4.27 / USD $4.65. However, Spotify also obviously just raised its US prices by between 6% and 20% across various tiers – with a 10% rise for its flagship individual price. We’ve applied this 10% uplift to the global ARPU figure of USD $4.65, which brings us to $5.12 per month.

Credit: QuiteSimplyStock/Shutterstock

The fun work

Imagine this scenario, then: Spotify cuts all ad-supported access to its service tomorrow in the US and Canada.

Those ~48.6 million free users of the service in these markets (as of the end of Q2) are told: Start paying, or clear off.

Question: How many ex-free users would Spotify need to convert to paying users to make up the shortfall in advertising money immediately lost from this move?

Answer: Remember – we’re assuming here that Spotify is currently generating USD $220 million from ad-supported users (i.e. ads) per quarter in the United States – or $73.3 million per month. We’re also assuming that the monthly ARPU of US-based paying Spotify subs now sits at $5.12.

Spotify would therefore have to convert 14.3 million of our assumed current ‘free’ active user base in the US and Canada (48.6m) to Premium in order to offset the revenue loss from exiting ‘free’ in these markets. That’s just under a third (29%) of its current free user base in North America.

A challenging prospect.

However, making small tweaks to these estimated numbers makes a significant difference.

For example, what if Spotify’s real (unpublished) ARPU figure in the US was more like $6.12 per month, rather than the $5.12 figure we’ve run with so far?

(Remember: Our $5.12 figure is rooted in the global paying monthly ARPU figure of Spotify as per its Q2 report, and the real US/Canada-only figure should, by logic, be significantly higher than this.)

If the $6.12 monthly ARPU figure came into play, Spotify would only need to convert 12.0 million current free users into paid users – less than 25% of its current ‘free’ user base in the US and Canada.

If its US monthly ARPU was $8.12, it would only need to convert 9.0 million current free users into subs – just 18.5%of its current ‘free’ user base in North America.

Which all begs the question: WHY, exactly, might Spotify seriously consider making such a move in future – especially when the US is the epicenter of the global digital ads market?

There are three main arguments weighing in the favor of Daniel Ek and co. doing so.

Argument 1: Spotify’s loss-making, troubled ads business

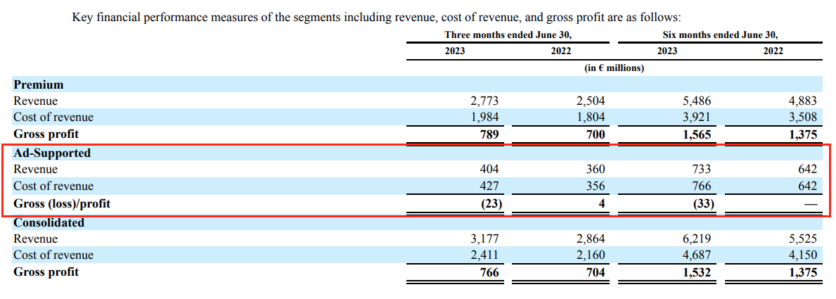

So far this year, Spotify’s ads business is loss-making on a gross margin basis.

In other words, it’s spent more money on the basic costs of generating ad revenue than it’s actually generated from ad revenue.

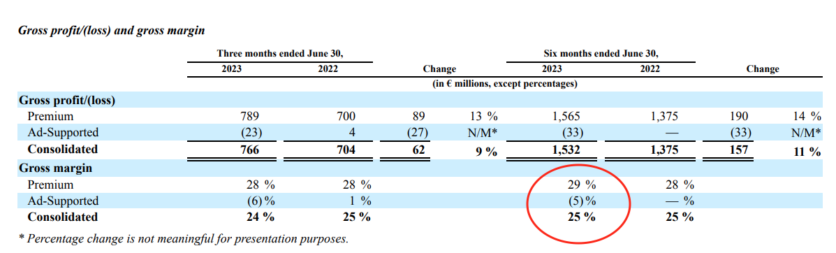

In the first six months of this year, Spotify posted a negative gross margin (aka a ‘gross loss’) of EUR €33 million for its ad-supported business (see below).

To be fair, Spotify’s SEC filings show its most significant ad-revenue quarter is in Q4.

As such, annually, Spotify’s gross profit has recently turned positive, but it’s still razor-thin: In FY 2022, Spotify’s ad-supported gross profit was just €30 million.

Obviously, this is ad-supported gross profit. That, says Spotify’s filings, includes the money the firm spends on podcast content.

But it doesn’t include vast operating costs – including sales & marketing and research & development.

All of this, in turn, is dragging down Spotify’s overall gross margin.

Without its ad-supported business, Spotify’s global gross margin in H1 2023 (i.e. the % of total revenue made up by its gross profit) would have been 29% (see below).

Dragged down by its ad-supported business, the firm’s gross margin in this period actually ended up at 25%.

Spotify analysts have been baying for improved gross margin figures from the firm ever since it floated on the NYSE in 2018 – and continue to do so.

Conversely, Spotify’s Premium (subscription) business is comfortably gross-profitable.

In the first six months of 2023, it generated a gross profit of €1.565 billion. In FY2022, that Premium gross profit stood at €2.896 billion.

The gross-profitability of Spotify’s Premium business is especially significant because gross profit is calculated after ‘cost of revenue’ is deducted. In the case of Spotify Premium, ‘cost of revenue’ includes the ~70% of revenue that SPOT pays out to music rightsholders.

Overall, of course, Spotify’s subscriptions business continues to tower over its ads business globally.

In the first half of 2023, 88.2% of Spotify’s €6.219 billion total global revenues were generated from Premium subscriptions, with ad revenues only contributing 11.8%.

In the full year of 2022, 87.4% of Spotify’s €11.727 billion total global revenues were generated from Premium subscriptions; ad revenues only contributed 12.6%.

And, proving these stats aren’t a product of recent macroeconomic headwinds for the digital ad market, ad-supported revenues at Spotify made up a similarly small proportion of total FY global revenues in both 2021 (12.5%) and 2020 (9.5%).

Argument 2: Losing ad-supported doesn’t have to mean losing ads

One of the key arguments against Spotify scrapping its ad-funded tier in the US is that it would be throwing away a golden opportunity.

Its ad-supported business might be losing money today, goes the logic, but commercial glory is there for the taking in the decades ahead.

The United States is the world’s biggest ads market, with an estimated $245 billion spent on digital ads last year (although nearly 50% of that was jointly eaten up by Meta and Alphabet).

Projections suggest that this annual US digital advertising spend figure could reach $397 billion by 2027.

Yet if Spotify scrapped its entire ad-supported business in the US tomorrow, there would still be another route to generating ad revenue on its platform – by following in the footsteps of Netflix.

In November last year, Netflix launched a lower-priced (‘Standard with ads’) subscription tier, costing $6.99 per month in the US, on which consumers are served advertising.

A totally ad-free Standard subscription on Netflix today costs more than double this price, at $15.49 per month.

Is this ‘Standard with ads’ lower-priced subscription model something Spotify could emulate – a model whereby income from your lowest-paying customers is subsidized by additional ad revenue?

By May this year, Netflix’s ‘Standard with ads’ tier had racked up nearly 5 million active global users per month, according to the company.

In its latest earnings announcement, Netflix said this figure had “nearly doubled since Q1”.

However, the firm further clarified via its Q2 2023 earnings that ad revenue being generated by its ‘Standard with ads’ business wasn’t currently “material” to its global business.

It added: “Building an ads business from scratch isn’t easy and we have lots of hard work ahead, but we’re confident that over time we can develop advertising into a multi-billion dollar incremental revenue stream.”

“we have lots of hard work ahead, but we’re confident that over time we can develop advertising into a multi-billion dollar incremental revenue stream.”

Netflix investor letter on its ‘Standard with ads’ tier, July 2023

One other way Spotify could continue to earn advertising money even if it dumped its free tier tomorrow? Podcasts.

‘Premium’ subscribers on Spotify are today – despite being promised an ‘ad-free’ music experience – still subjected to listening to sponsorships of podcasts.

Spotify doesn’t break out within its SEC filings exactly how much of its current advertising revenues are from podcasts, but its Q2 2023 filing did reveal: “Ad sales from podcasts… increased [in] revenue by €15 million during the three months ended June 30, 2023.”

Argument 3: The subscription market in the US is running out of headroom – and the ‘carnivores’ are coming

This is the idea that, in the US, music is edging toward a point of streaming subscription growth maximization. Or to put it less poetically: When everyone who is willing to subscribe to a music streaming service is already doing so.

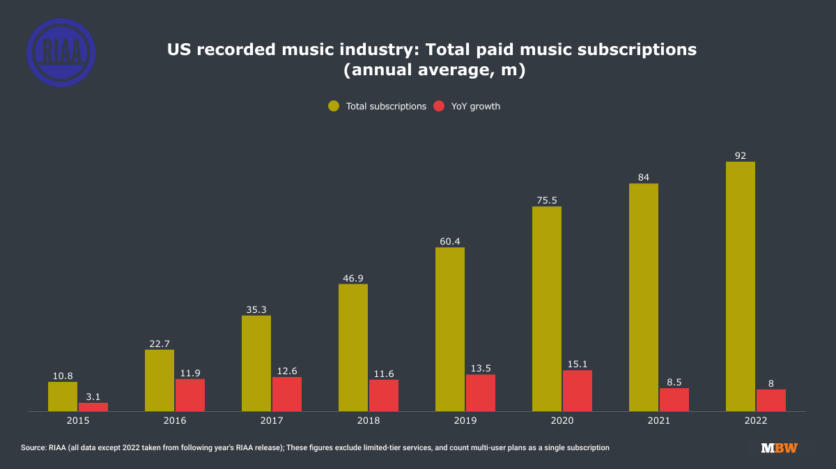

Fuelling this suspicion: According to the latest RIAA figures, in 2022, there were +8 million more paying music streaming subscribers in the United States than there were a year before.

That was down slightly on the +8.5 million YoY gain we saw the year before (2021), and down significantly on the YoY increase we saw in both 2020 (+15.1m) and 2019 (+13.5m, see below).

This YoY growth figure is expected to continue getting smaller in the years ahead, as the US subscription market – at least in terms of volume of subscribers, as opposed to volume of revenue – hits a natural saturation point.

The economist Will Page – formerly Spotify’s Chief Economist – has argued that ‘Peak Subscription’ in the US may be here quicker than most people think.

The tipping point? Page estimates that there are only 110 million ‘qualifying households’ in the States in terms of potential paying streaming customers.

We’re already at 92.0 million individual paid-subscription accounts in the territory, according to the RIAA. (Important: that’s subscription accounts, not users of subscription accounts.)

This near-saturation, Page suggests, will ultimately see the ‘herbivore’ behavior of music streaming services in the United States today transform into ‘carnivore’ behavior. i.e. When there are no more un-converted music streaming subscribers available in the US market, streaming services will switch their focus to stealing each other’s customers.

Within Spotify’s annual report, it part-justifies its ad-supported tier’s existence with the following words: “Our Ad-Supported Service serves as a funnel, driving a significant portion of our total gross added Premium Subscribers.”

That argument struggles to hold water in territories where there are no new Premium subscribers to attract – except, perhaps, your own existing ‘free’ users.Music Business Worldwide